Everyone has some idea of what it means to be money smart – however, whether or not you’ve acted on that idea is a different story! There are a few nuggets of financial wisdom that have become clichés, albeit practical ones. Curb your spending. Pay off your debt. Contribute to your savings early and often. Compound Interest is your friend. Start saving now and watch your money grow.

Being financially responsible starts with putting some of those clichés into action, but in doing some research into saving strategies, you might be in for an unpleasant surprise. You might do some quick calculations with current interest rates and come to the sobering realization that the effects of saving your money aren’t as mind-blowing as you thought. Why is that?

The economic landscape has changed a lot in the past 20 years. Our parents saw a time where it was possible to put your money away in a certificate of deposit (CD) with interest rates upwards of 10%. Strategically utilizing investments with that kind of return was a smart move and a great way to grow your money over time.

Unfortunately, those days of 10% interest rates seem to have disappeared along with the era of acid-wash jeans and Troll dolls. Current interest rates are at historic lows, and the Federal Reserve predicts that the trend is going to stick around for a while. Saving is, of course, still a crucial part of your financial well-being, but what’s the best way to grow your money and beat inflation when interest rates are low? Consider the following strategies:

Check Your Expectations.

There’s no way to sugarcoat it; interest rates are low right now. As a result, your investments – even with the mighty power of compound interest – just aren’t going to perform as well as they would have in the past.

Countering the effects of inflation is another resulting challenge. But don’t get too discouraged—as a young investor, time is on your side.

Even low-yield investment products can generate significant wealth over long periods of time (we’re talking decades), but it’s important to stay realistic with your long-term savings goals.

Will your investment allow you to buy your own island when you retire? It’s highly doubtful, but with some foresight and planning, your investment can allow you to retire comfortably and with peace of mind.

The rich gets richer and the poor poorer. Most of the time, the missing link is “information.” The wealthy people know something that average people don’t and that is financial education. One of the secrets of the wealthy is that they know how to let money work for them.

However, most of us don’t know how to let money work, thus we work hard for the money. But the challenging part is that nobody wakes up at 6 or 7 am and says, “yehey! It’s time to go to work!” Unless we know how to let money work, we are doomed to work for the rest of our lives. So how does money work?

Money works through the help of interest rates. There are two types of interest rates: Simple and Compounding Interest.

Simple Interest:

Example: 1% interest on the principal per year.

100 (principal savings)

After 1 year: 101

After 2 years: 102

After 100 years: 100 becomes 200! Exciting!

Compound Interest:

Understanding the magic of compound interest:

Example: 1% interest compounded annually

100 (principal savings)

After 1 year: 101

After 2 years: 102.01 (because your 1 peso also earns 1% interest)

After 3 years: 103.03 (the magic of compounding!)

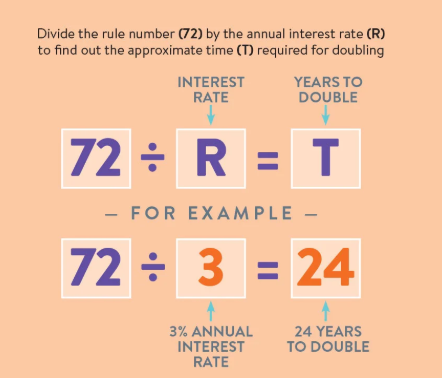

Experts have derived a simple formula to estimate the number of years your money doubles through compounding called the “Rule of 72.” The rule states that 72 (constant) is divided by the interest rate per year equates to the number of years your money will double.

72 / i = # years money doubles

Using the values above, 72 / 1% = 72 years.

Therefore: 100 becomes 200 after 72 years (compared with 100 years in simple interest rates)

Another interesting thing to note about the magic of compounding: small changes in the interest rate = millions in the end result of your savings.

Example: 100,000 invested in 4%, 8% and 12% at age 29. Using the rule of 72, the number of years your money will double is 18, 9 and 6 years, respectively. At retirement age of 65, see the big difference below.

Obviously, the bigger the interest, the bigger the result. But the not so obvious beauty of compounding is, the difference between 4 and 8% is 2 times but the difference of 400K and 1.6M is four times! The difference of 4 and 12% is thrice but the difference of 400K and 6.4M is 16 times!!! Now that is very powerful!